| TL;DR: With new “fully agentic” and “industry-first” announcements arriving every few weeks, how should credit union CEOs, COOs, and contact center leaders evaluate an agentic AI vendor in 2026? This article walks through the three questions that matter: channel coverage, production outcomes, and what happens when the vendor’s strategy shifts. Explore 2026 research from Cornerstone Advisors and deployment stories from real credit unions. |

“The board wants an answer by next month. Which vendor are we actually choosing?”

“There are three launches on my desk from the last six weeks. All of them say ‘industry-first.'”

“Fine. Which one has a credit union our size running it in production today?”

“That’s the question, isn’t it?”

If that conversation sounds like one you have already had this quarter, you are not alone. CEOs, COOs, and contact center leaders at credit unions across the country are fielding the same questions from their boards, their operations teams, and sometimes their members.

The agentic AI category has gone from emerging to crowded in under a year. Every few weeks, another vendor arrives with a launch that claims to redefine the category.

The truly critical question to consider is not which vendor creates the most noise, but rather which one has active production deployments that mirror your own environment.

Why “Proof Is The Product” Matters Right Now

The market data has shifted fast, and the numbers are worth reading twice.

Cornerstone Advisors’ What’s Going On in Banking 2026, based on a survey of 416 senior executives, found that 59% of credit unions have already deployed generative AI. That figure gives credit unions a 10-point lead over banks at 49%.

On agentic AI specifically, the lead is sharper. 17% of credit unions are investing in agentic AI, more than double the 7% at banks. The contact center is the top use case.

Furthermore, 74% of credit unions apply generative AI to the contact center, ahead of fraud, lending, marketing, and IT.

Credit unions are not deliberating. They are deploying.

Vendor selection has become a higher-stakes question because of that shift. When an institution moves from pilot to production, the cost of picking the wrong platform compounds across multi-year contracts, member experience, and operational strain.

Ron Shevlin, Cornerstone’s chief research officer, framed the 2026 distinction in plain terms.

“What separates leaders from laggards in 2026 won’t be who experiments the most, but who operationalizes these technologies with discipline and purpose.”

The same discipline applies on the vendor side. A product is what it does on a Tuesday morning at a credit union like yours. Everything else is positioning.

When evaluating any agentic AI vendor in 2026, ask three questions.

- Channel coverage.

- Production outcomes.

- Long-term vendor risk

A “Fully Agentic CCaaS” Must Cover All The Channels Your Members Already Use

Start with the channels members actually use, because that is what the contact center exists to serve.

- A credit union member’s day does not happen in one channel

- A loan question starts in SMS

- It turns into a voice call

- And it finishes in a video banking session the next morning with a loan officer who shares a screen and walks through the application

- The agentic platform worth buying is the one that holds a single authenticated conversation across all of those moments, a unified conversation platform.

Many of the newer agentic CCaaS products launching this year cover two channels at debut: voice and chat.

That is a reasonable starting point; however, it is not a complete platform. Before signing with any vendor, confirm what the launched product handles natively now, not what is on the roadmap.

The checklist is short and worth printing:

- Voice and chat in one session (table stakes)

- Native SMS that is TCPA-compliant

- Native video banking, not a third-party integration

- Screensharing and co-browse during the same authenticated session

- Session continuity across channels without asking the member to re-identify

Eltropy built the unified platform around this requirement from the beginning. The platform handles voice, chat, text, SMS, video, and screen sharing in one session, with authentication intact as the member moves between channels.

That architecture is not marketing.

It is the reason a member does not have to repeat an account number four times in a single interaction.

Production Outcomes Are The Only Credential That Matters

“Industry-first” is a phrase. Production evidence is a credential.

The difference shows up the moment you ask a vendor for three named customers running the product in production, at institutions your size, with senior executives willing to take a reference call.

Vendors with a deployed platform answer the question in the meeting. Vendors without one offer to follow up.

Consider Cobalt Credit Union. Nebraska-based, formerly SAC Federal Credit Union, serving a military-rooted membership stationed in every U.S. state and more than twenty countries. Cobalt’s agentic AI deployment was not a single announcement. It was a sequence that took years.

Video banking came first, through POPi/o, back when video was still the emerging channel. Chat followed. Then text messaging. Then AI, first for chat, then for voice.

At Eltropy’s EMERGE 2025 conference, Chasmine McIntosh, Cobalt’s VP of Digital Banking, said, “We do Chat, we do Text, obviously Video Banking. We have stood up our AI agents. So Coby (intent-based AI) speaks with our members. It gets rave reviews and is able to handle a lot. Right now, we have an 83% Session Containment Rate.”

On that note, Finovate’s editorial coverage noted that typical voice containment rates fall between 60% and 80%, which makes Cobalt’s outcome a measurable leading-edge result.

Cobalt’s voice assistant, Coby, is not a launch story. It is a deployment story.

The pattern holds elsewhere on the Eltropy platform.:

TruStone Financial’s AI chatbot,a $4.5B Minnesota-based credit union serving more than 200,000 members, deployed Eltropy’s AI chatbot to handle routine member inquiries across digital channels. It now independently resolves 46% of conversations, with members rating the experience 9.4 out of 10.

At Credit Union of Texas, the deployment went further. The COO reports that 90% of AI-handled interactions resolve without a human handoff, a containment rate that sits at the top of what Finovate benchmarks as leading-edge performance for voice AI in financial services..

Each of these outcomes is disclosed, attributed to a named executive, and available for reference. The broader platform now serves 750+ credit unions and community banks across North America.

A platform has production references a buyer can call this week. And a launch has a roadmap.

The Real Vendor Risk: What Happens When The Strategy Shifts

A vendor who entered 2025 as a digital customer service platform and is now repositioning as a CCaaS is not a stable architectural bet for a three-year contract. That is not a criticism of ambition. It is a structural observation: the buyer absorbs the cost of every strategic pivot the vendor makes mid-contract.

Contact center contracts run three to five years. Agentic AI vendor strategies are shifting in quarterly cycles. Those two realities do not mix well.

The category is moving fast, and vendor positioning is moving with it. A product marketed one way in one quarter may be marketed differently the next. That is not unusual for an emerging market.

Both positions can be defensible on their own. Both cannot be a durable commitment at the same time.

For the buyer signing a three-year contract today, the question is not which vendor will shift. Shifts are inevitable in a category this young.

The question is whether the architecture you are buying can absorb those shifts without forcing a migration.

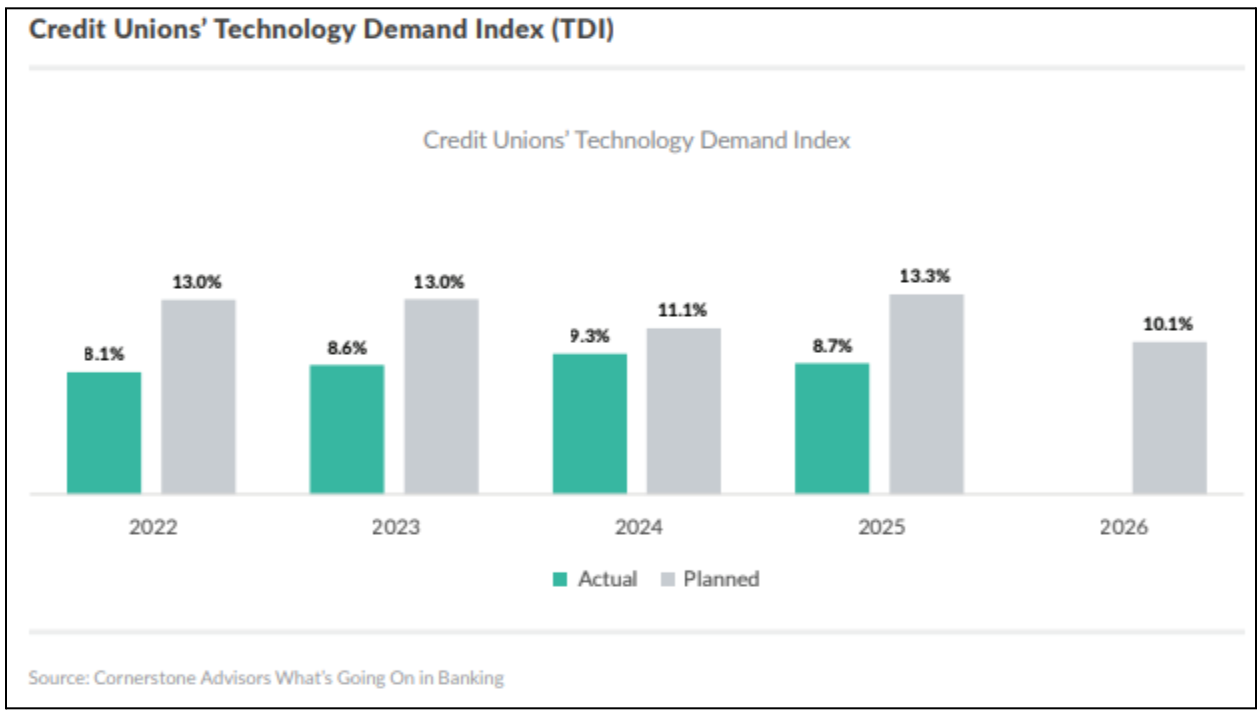

Let’s look at Cornerstone’s 2026 research that adds a useful frame on wrong vendor investment.

This index highlights the persistent “execution gap” within the credit union sector, where actual tech deployments (averaging ~8-9%) consistently trail behind ambitious planning. The projected dip in 2026 “Planned TDI” to 10.1% suggests a strategic pivot: credit unions are moving away from broad system replacements to focus on higher-impact, unified platforms to avoid the compounding costs of technical debt.

Contact center migrations are hard to unwind, and planned system replacements at CFIs often fall well short of actual deployments. That gap makes the cost of choosing the wrong vendor compound over years; architecture reduces that risk, but assertions do not.

A short question set for the next vendor briefing:

Does the platform allow third-party fintechs to build specialized agents on top of it?

How many named integrations does the vendor have with your core, LOS, digital banking, and CRM?

What happens when I have multiple vendors that don’t plug into each other at all?

What is the AI governance framework for agent actions?

What industry-body endorsements does the vendor carry?

What is the vendor’s current SOC 2 Type II audit window, and which Trust Services Criteria are in scope?

If a vendor can’t answer these in the room, that is the answer. For the record: Eltropy’s platform was built to answer every one of them. Third-party agents like Constant AI‘s Skip-A-Pay build directly on top of it. Fifty-plus core, LOS, and CRM integrations are disclosed and named. The Safe AI Framework governs every agent action with defined access controls and approved SOPs. SOC 2 Type II and PCI DSS attestations are current. And the reference calls are real, credit union executives, available this week.

On The Wrap Up: What CFI Leaders Should Do Next?

The announcement cycle will not slow down. Every quarter in 2026 will bring another “world’s first” in some dimension of agentic AI for CFIs. The discipline is not cynicism about new products.

It is the consistency in the questions you ask.

The pressure to decide is not manufactured. The PYMNTS 2026 Credit Union Tracker, with Velera, reports that 80% of Gen Z and younger millennial consumers use AI for financial planning, and roughly three-quarters are comfortable with agentic AI. The members have already moved. The contact center has to catch up to them.

Three questions. The same ones every time.

- Does the platform cover the channels your members actually use today?

- Can the vendor show you named production deployments at credit unions like yours?

- And do you understand what happens to my operations if the vendor’s strategy shifts?

Proof is the product.

The credit unions that ask for it, and the vendors that can produce it, are the ones that will win 2026.